Loan Agreement

About Loan Agreement

The Loan Agreement template by Skala is a simple, no-nonsense way to document a loan between a founder and their own company (or anyone else, really). It sets out the loan amount, repayment terms, interest (if any), and governing law in a format that’s actually readable.

One of the most common early-stage funding sources is a founder reaching into their own pocket. This template is made for exactly that: lending money to your company to get it off the ground, before the revenue, before the raise, and ideally before your first tax reporting period turns into a spreadsheet headache.

It’s for founders, investors, and teams who want to make things official without making things complicated.

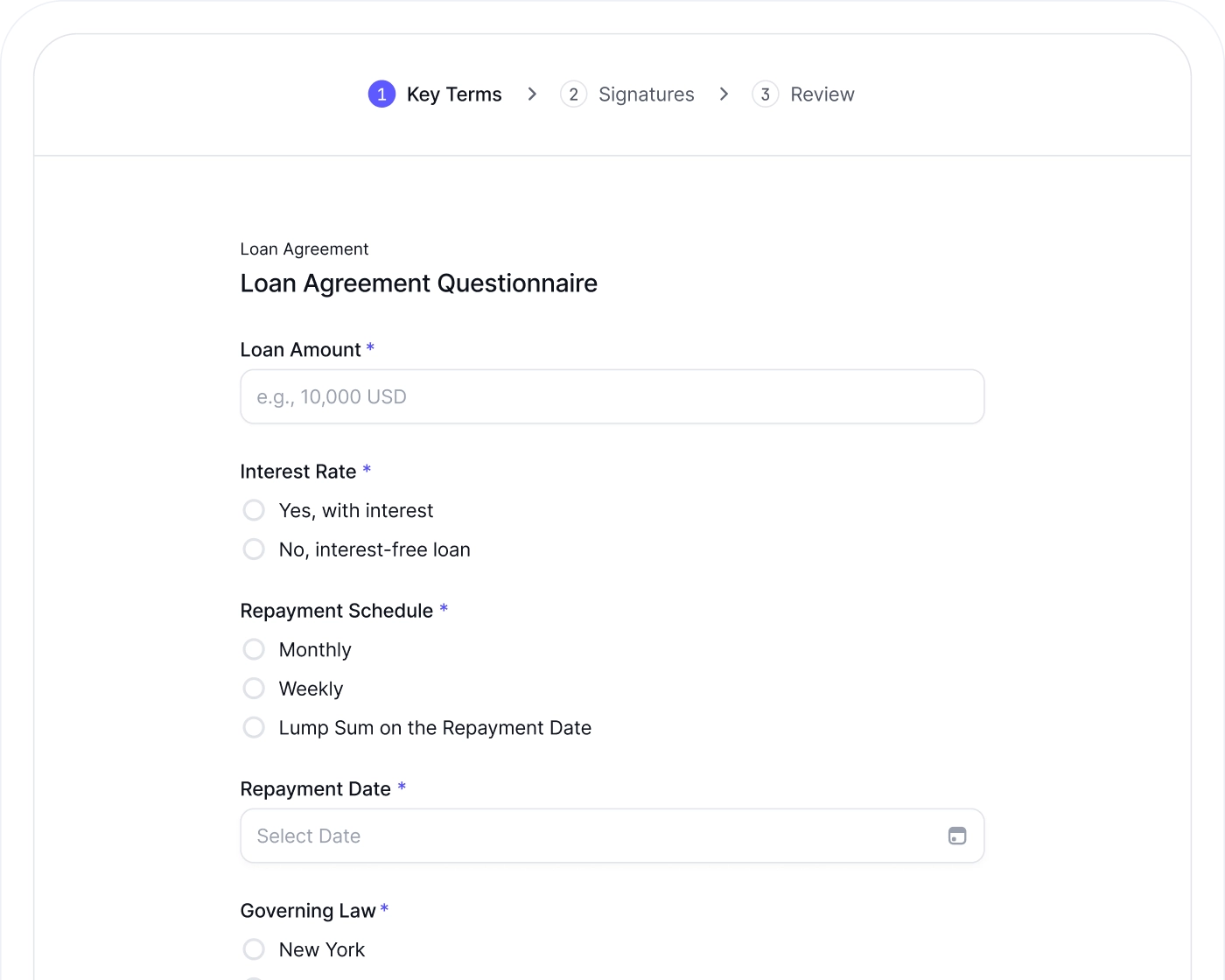

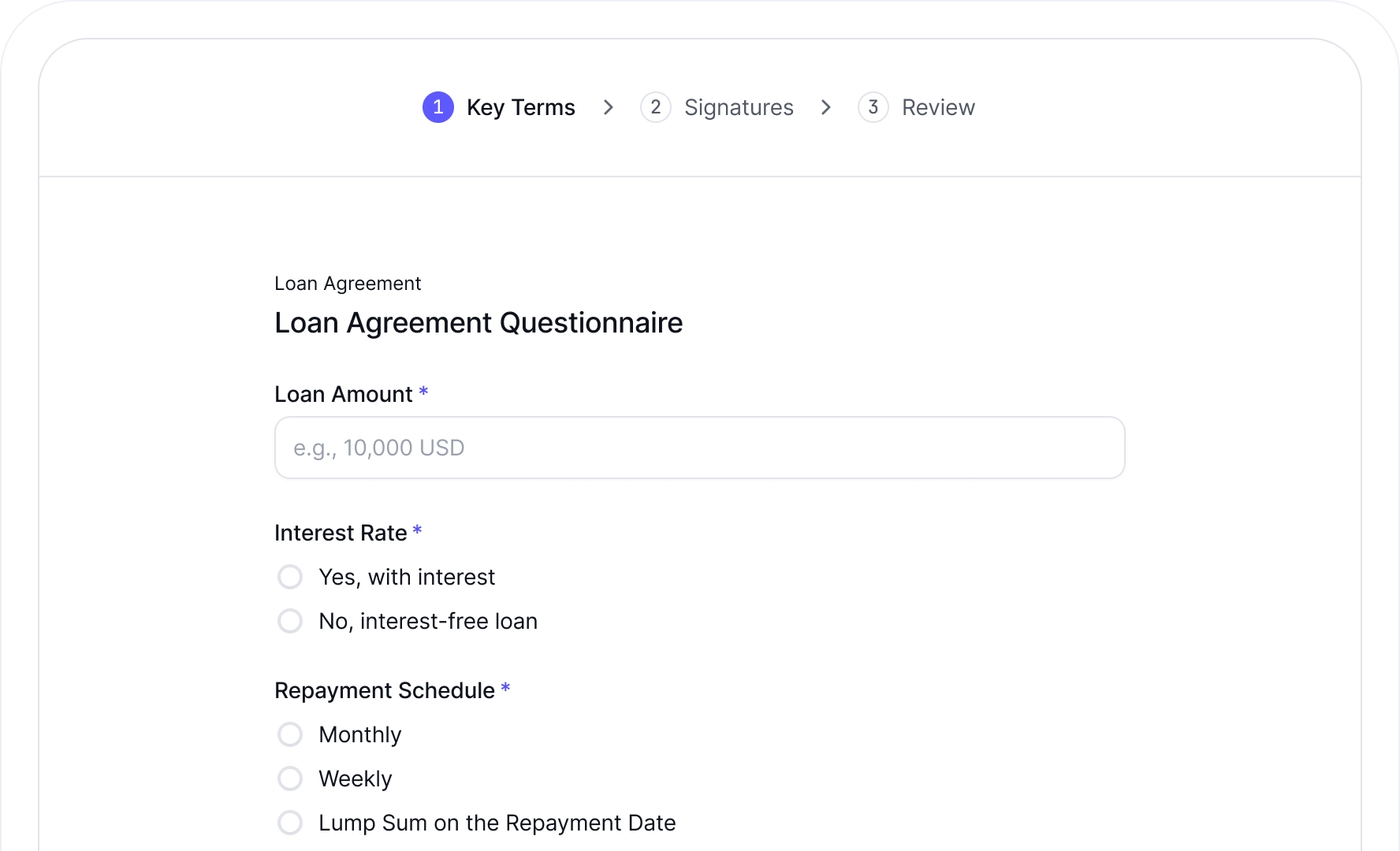

What’s Inside

This template covers all the usual suspects: how the loan gets sent, how it gets repaid, what happens if it doesn’t, and what law governs it all. It’s designed to work in practice, not just look good in a folder.

Loan Disbursement

The lender wires the money within 5 business days. Each transfer gets its own timestamp and treatment as a separate disbursement. Everyone pays their own fees. No drama, no surprises.

Repayment Obligations

You can include an interest rate, or not. You can set a fixed schedule, or leave it open. Borrowers can repay early any time, with zero penalties and zero side-eye.

Events of Default

Miss a payment? File for bankruptcy? Shut down operations? That triggers immediate repayment. No need for courtroom suspense, everything’s spelled out.

Term and Termination

The agreement kicks in on the effective date and lasts until the loan is fully repaid. If both parties want to extend the term, just put it in writing. Easy.

No Assignment

Neither party can hand off their obligations to someone else unless it’s part of a merger or asset sale. This keeps control in the hands of the original players, which is usually where it belongs.

Governing Law

You get options: New York, UK, Singapore, UAE, or “Other.” Use UAE only if there’s no interest rate. We don’t make the rules, but we do try to follow them. In general, pick the law that actually has something to do with your business.

One document. Countless deals.

FAQ

The exercise price of the shares under the FAST agreement will be determined at the time of issuance and will be included in the applicable Stock Purchase Agreement.

-

-

-

-

-

FAQ

Because without a written agreement, the IRS or a future investor can recharacterize the transfer as a capital contribution — meaning you gave the company money as equity, not debt, and you may not be able to take it back without a dividend or stock buyback. A signed loan agreement establishes that the transfer is debt: repayable, potentially interest-bearing, and separate from your equity stake. It also protects you in due diligence — investors routinely ask to see how founder loans are documented, and a missing or informal record is a red flag. The short version: a one-page agreement now prevents a much larger headache later.

A loan agreement should clearly state the loan amount, disbursement date, interest rate (if any), repayment schedule, and final repayment date. It should also explain what happens if the borrower defaults, including whether the lender can demand immediate repayment. Depending on the loan, the agreement may also cover prepayment, late payments, collateral, governing law, and how amendments must be made.

Not always. The parties can agree on an interest-free loan, but this depends on applicable law. In the U.S., related-party or below-market loans may trigger imputed interest or tax issues unless they use at least the applicable federal rate. In some jurisdictions, including the UAE, interest on private or non-commercial loans may be restricted, so the agreement should clearly state whether interest applies and reflect the chosen governing law.

The agreement should specify the consequences: a grace period (if any), late fees, and when a default triggers acceleration — meaning the entire outstanding balance becomes due immediately. The lender should also retain the right to pursue legal remedies and, in a secured loan, to enforce against the collateral. Clear default and acceleration provisions reduce uncertainty and make the agreement significantly easier to enforce.

Yes, by mutual written consent. Both parties must agree to any changes — extending the repayment date, adjusting the interest rate, or modifying the payment schedule. Oral modifications are rarely enforceable for loan agreements. Any amendment should be signed by both parties and attached to the original agreement as a written addendum, clearly stating which provisions it replaces.

Launch Your Business with Confidence

Start for Free with Skala

Migrate it to Skala for maintenance

We will notify you of important deadlines

Impress your investors and get money fast

Import your actual and pending trademarks free of charge

Quickly generate NDAs, onboard contractors without hustle

We will help you with getting a bank account

Legal quizzes and guides

Access special offers and perks from our partners

If you need one, we'll get you introduced in no time